Rotas built from habit

Copying last week’s rota without checking sales forecasts can create hidden overstaffing.

Learn how restaurant labour cost works, how to calculate labour cost percentage, what healthy staffing benchmarks look like and how to control payroll without damaging service quality.

Restaurant labour cost is the total amount a hospitality business spends on staffing. It includes wages, salaries and the employment costs connected to running the team.

For operators, labour cost is not just an accounting number. It affects rota planning, service quality, team productivity, customer experience and profitability. A restaurant can be busy and still lose margin if staffing is not planned around realistic sales.

Restaurant labour cost is the cost of the people needed to operate the business, serve guests, prepare food, manage shifts and keep the venue running.

Labour cost percentage shows how much of your sales revenue is being spent on staffing. It is one of the clearest ways to understand whether your rota is aligned with revenue.

Labour Cost Percentage = Total Labour Cost ÷ Total Sales × 100

For example, if your restaurant spends £7,500 on labour and generates £25,000 in weekly sales, labour cost percentage is 30%.

To calculate this faster before finalising a rota, use the free Staff Schedule & Labour Cost Calculator.

A good labour percentage depends on the type of venue, service model, pricing and opening hours. Quick service venues usually need lower labour percentages than full-service restaurants or fine dining operations.

| Business type | Typical labour cost range | Why it varies |

|---|---|---|

| Quick service restaurants | 20% – 30% | Lower service complexity and faster production systems. |

| Cafés and coffee shops | 25% – 35% | Labour depends heavily on peak periods, prep and service style. |

| Casual dining | 25% – 35% | Front-of-house and kitchen labour both affect service delivery. |

| Fine dining | 30% – 40% | Higher service expectations and more labour-intensive delivery. |

For a deeper benchmark explanation, read What Is a Good Labour Cost Percentage for a Restaurant?.

Most labour cost problems start before anyone arrives for their shift. Weak forecasting, repeated rotas and no reaction to changing sales quietly push staffing costs above where they should be.

Copying last week’s rota without checking sales forecasts can create hidden overstaffing.

If too many hours are scheduled for the revenue generated, labour efficiency drops quickly.

Overtime usually points to rota gaps, late finishes, weak prep planning or poor cover.

Reducing labour cost should not mean cutting staff blindly. Poor cuts can damage service, increase pressure on the team and reduce sales. The better approach is to remove waste from the rota while protecting the shifts where guests actually need service.

For the full playbook, read How to Reduce Restaurant Staffing Costs Without Hurting Service.

Labour cost and payroll cost are closely connected, but they are not always the same thing in day-to-day restaurant management. Payroll usually describes what is paid to staff through wages or salaries. Labour cost should give a fuller operational view of what staffing actually costs the business.

For accurate planning, restaurant managers should include the costs attached to employment, not only the hourly wage on the rota. That means holiday pay, employer contributions, overtime, salaried management and temporary cover should be considered when reviewing true labour cost.

A rota can look affordable if you only count hourly wages, but become expensive once employer costs, holiday cover and overtime are included.

This matters because small errors in payroll planning repeat every week. A few unplanned hours per day, a supervisor finishing late or regular overtime on closing shifts can quietly move labour percentage above target even when sales look healthy.

Not every labour hour behaves the same way. Some staffing is fixed because the business needs a minimum team to open safely, prepare the venue and complete essential tasks. Other staffing is variable because it should change depending on sales, covers, bookings, delivery volume or expected footfall.

Managers, openers, closers, prep staff and minimum kitchen or front-of-house cover required to operate.

Extra team members added for peak periods, events, bookings, delivery demand or expected sales volume.

The biggest savings usually come from matching variable labour to real demand without weakening core service.

Separating fixed and variable labour helps managers avoid the wrong type of cost cutting. If core cover is cut too aggressively, service quality drops and the team becomes stressed. If variable labour is not adjusted when sales are lower than expected, the rota becomes inefficient.

A labour budget gives managers a target before the rota is written. Instead of building a schedule first and checking the cost afterwards, the better approach is to start with expected sales and decide how much labour the business can afford.

For example, if a restaurant expects £30,000 in weekly sales and wants to keep labour at 30%, the labour budget is £9,000. The rota should then be planned around that limit, with enough flexibility to protect busy shifts and reduce unnecessary cover during quieter periods.

Labour Budget = Forecast Sales × Target Labour Percentage

The goal is not to hit the budget perfectly every week. The goal is to give managers a clear number before decisions are made, so staffing becomes planned instead of reactive.

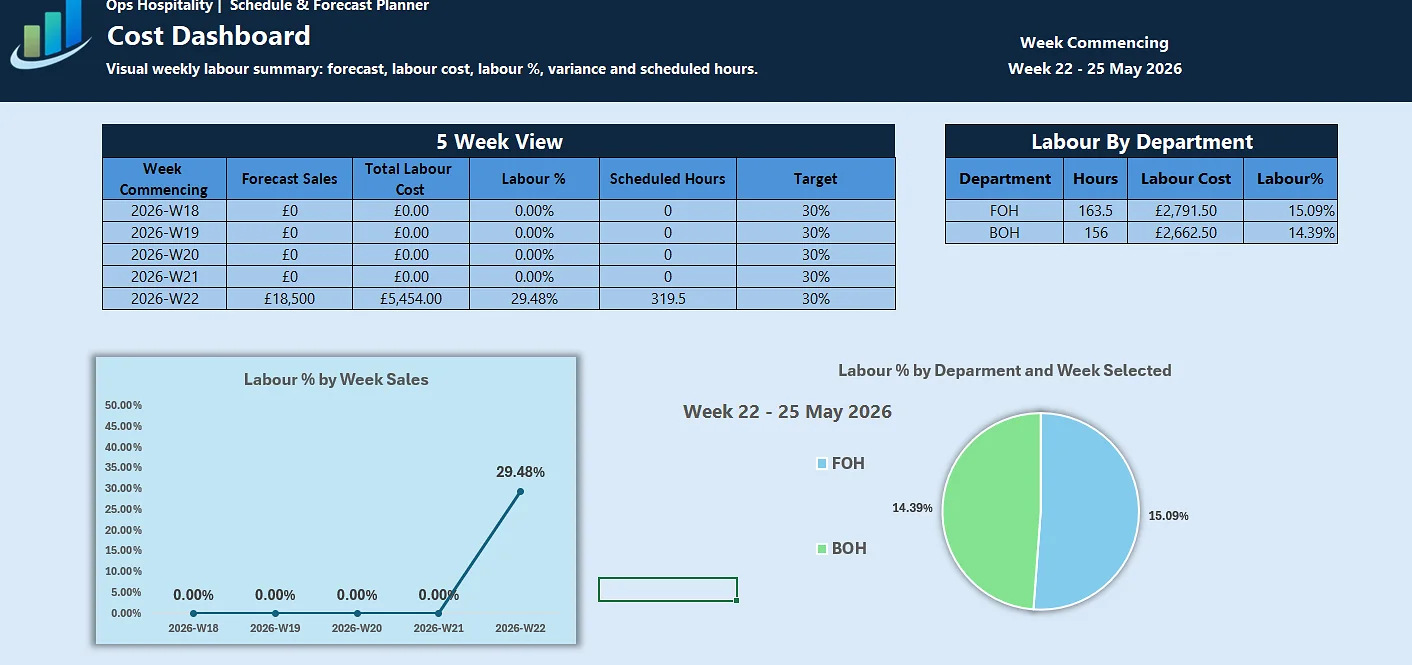

If you want to plan labour before the week starts, use the Schedule & Forecast Planner to connect weekly schedules, forecast sales, scheduled hours and labour cost in Excel.

View Schedule PlannerWeekly labour cost is useful, but daily tracking is what helps managers react in time. If labour is only reviewed after payroll is complete, the opportunity to fix the problem has already passed.

Daily labour tracking compares actual sales and actual labour spend against the target. This helps managers spot whether the team is overstaffed, whether sales are below forecast or whether hours are creeping up through late finishes and unplanned cover.

Review bookings, weather, events, delivery expectations and sales targets before the day starts.

Compare actual trade to expected trade and adjust breaks, starts or finishes where possible.

Check actual labour cost against sales so the rest of the week can be adjusted early.

This does not need to be complicated. Even a simple daily review of sales, labour hours and labour percentage can improve control because managers stop waiting until the end of the week to understand performance.

Many restaurants do not lose control of labour through one big mistake. The issue is usually a series of small habits that repeat every week and slowly make the rota more expensive than it needs to be.

The best labour control systems are simple, visible and used consistently. Managers need to know the target, understand the forecast and have enough information to adjust before the week is over.

Labour cost should not be reviewed alone. In restaurants, labour cost and food cost together form prime cost. Prime cost is one of the strongest indicators of whether a venue is operationally sustainable.

Prime Cost = Labour Cost + Food Cost

A restaurant with slightly higher labour cost may still perform well if food cost is controlled and sales are strong. But when both labour and food cost are high, profitability becomes difficult to protect.

Read more: What Is Prime Cost in a Restaurant? or use the Restaurant KPI Calculator to review labour cost, food cost and prime cost together.

Plan weekly rota cost, employer cost, labour percentage and monthly payroll impact.

Open tool →Plan weekly schedules, forecast sales, scheduled hours and labour cost in Excel.

View template →Track labour percentage, food cost, prime cost and profitability in one place.

Open tool →Understand healthy labour targets by restaurant type and service model.

Read guide →Practical ways to reduce labour pressure while protecting service quality.

Read guide →Learn the performance metrics hospitality managers should track.

Read guide →Restaurant labour cost is the total cost of staffing the business, including wages, salaries, employer costs, holiday pay, overtime and other employment-related expenses.

Divide total labour cost by total sales, then multiply by 100. For example, £7,500 labour cost divided by £25,000 sales equals 30%.

Many restaurants operate between 25% and 35%, but the right target depends on concept, pricing, service level and operating model.

Restaurants can reduce labour cost by improving sales forecasting, building smarter rotas, reducing overtime, cross-training staff and tracking labour daily.

Yes. For a realistic view of payroll impact, labour cost should include employer contributions, holiday pay, overtime and other staffing-related expenses.

Build a weekly rota, estimate payroll impact and understand your labour percentage before staffing costs get away from you.